Seasonal Beef Demand

Derrell S. Peel, Oklahoma State University Extension

Wholesale beef prices have moved higher thus far in 2026, reflecting both strong beef demand and typical seasonal patterns.

Choice boxed beef prices averaged $386.41/cwt. the first week of March, up 9.1% from the beginning of the year, and up 23% year-over-year.

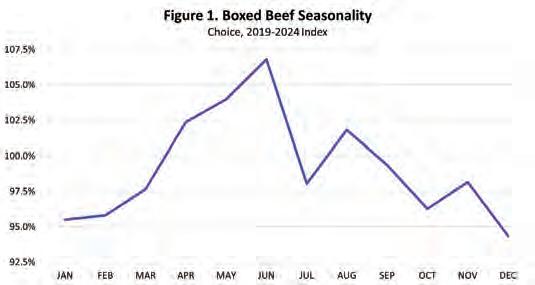

Boxed beef prices normally increase through the first half of the year, peaking in June, before declining to the end of the year (Figure 1). Boxed beef prices usually begin to increase more sharply in April as retailers build inventories for the coming summer demand that begins in late May. The average seasonal price index indicates that boxed beef prices typically increase by over 11% in the first half of the year. This year, boxed beef prices have already increased over 9%, earlier than usual. It is not clear if boxed beef prices will increase more than seasonally this year or simply move to seasonal peaks sooner than usual. Both are possible.

The boxed beef seasonal price pattern in Figure 1 is the net effect of many beef products included in the composite boxed beef measure. Across many beef products from the various carcass primals, different beef products have varied and unique seasonal price patterns reflecting different seasonal demands. While many beef product prices are increasing in the first half of the year, some products have lower prices early in the year and higher prices later in the year.

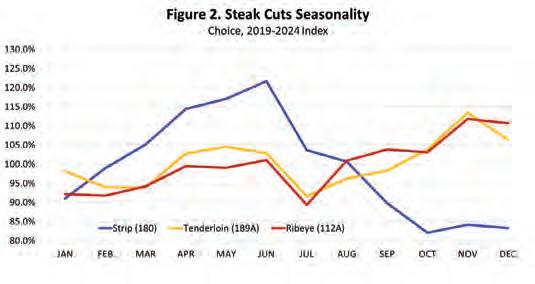

Figure 2 shows the seasonal price pattern for three middle meat cuts. High-valued middle meats drive much of the seasonal increase in cutout values. Strip loins lead the seasonal increase with the most variable seasonal pattern of any wholesale beef product, increasing an average of 30% from January to May. Strips are a popular summer grilling item as well as for restaurant menus. Ribeye prices also increase modestly in the first half of the year due to seasonal retail along with food service demand. Tenderloins are more popular for food service menus and the seasonal bump in the second quarter may be largely due to Mother’s Day demand. Prices of these steak items drop in the heat of summer with ribeye and tenderloin demand rebounding to seasonal peaks in the fourth quarter due to restaurant and holiday demand.

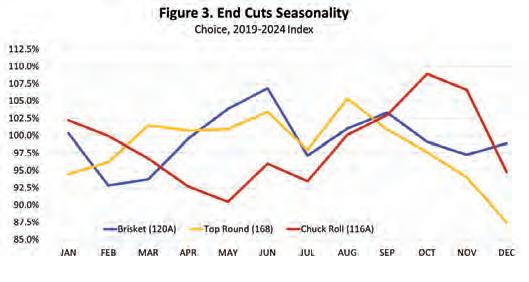

Figure 3 shows the seasonal price patterns for some end cuts and briskets. Brisket prices typically increase and peak in the second quarter with stronger summer demand. Round values have been very strong the last two years as a result of declining nonfed beef production and demand for additional lean. Round prices are typically strong from the second quarter through the third quarter as a result of seasonal ground beef demand. Prices for chuck rolls usually decrease into warmer weather. Chuck products have higher demand for roasts and crock pot cooking in cooler weather with prices reaching a seasonal peak in the fall. Chucks are also popular export items.

All wholesale beef cuts are higher year-over-year with most following seasonal patterns thus far in the year. The boxed beef cutout has increased faster than seasonally normal and suggests that beef demand remains strong in the face of tightening beef supplies.

Beef-on-Dairy is Becoming a Bigger Engine for the Beef Supply Chain

by Taylor Leach, Bovine Veterinarian

Beef-on-dairy has become a significant part of the US beef supply over the past decade, gaining momentum much like a freight train that keeps picking up speed. In fact, roughly 20% of today’s beef now traces back to a dairy cow, reflecting how integrated dairy production has become with the broader beef value chain.

And according to Matthew Cleveland of ABS Global and Nick Hardcastle of Cargill North America, that momentum shows no signs of slowing down. “I think we’re all aware of the scope and magnitude of what beef-on-dairy has become and the significant role it plays within our beef supply chain today,” Cleveland noted during a panel at the 2026 National Cattlemen’s Beef Association conference.

He says the sector’s growth has also changed how the dairy and beef industries view one another. Rather than operating as separate segments, the lines between them have blurred. “The dairy business is a big part of the beef business,” Cleveland says. “I don’t even like to separate them now. We’re all in the beef business, and we value partnership with our dairy producers.”

As beef-on-dairy has expanded, more attention has turned to decisions made on the dairy, where breeding choices directly influence how those calves perform all the way through the beef system.

Breeding with the Beef End in Mind

In the early days of beef-on-dairy, breeding decisions were driven largely by convenience rather than genetic intent. Beef semen was often selected based on price and availability rather than how those genetics would fit the needs of the beef sector. “Before people really started thinking about beef sire genetics on dairy cows, there wasn’t much consideration for what those genetics actually were,” Cleveland says. “Most decisions came down to what semen was already in the tank or what was free. The main goal was simply getting the cow pregnant.”

That approach began to change as the industry started to see beef-on-dairy as a long-term genetic opportunity rather than just a reproductive tool. “We began looking at beef on dairy more seriously from a genetic improvement standpoint around 2012,” Cleveland says. “We started to see the signals that beef-on-dairy was growing.”

Not long after, dedicated breeding programs were being developed across genetic companies to address the needs of both dairy producers and the beef supply chain. Today, Cleveland says those programs continue to evolve, with commercial performance data feeding back into genetic evaluations to drive ongoing improvement.

From “Black Holsteins” to Beef-Calf Performance

During the early days of beef-on-dairy, crossbred calves exposed real challenges for the beef industry. Cleveland notes that many of these animals were simply viewed as “black Holsteins,” which cooled enthusiasm among packers. “If you think back to 2013–14, you were just trying to create a black calf,” he notes. “We weren’t seeing the performance that you would expect from a beef calf. And for a few years, I think that soured the supply chain on the idea of beef-on-dairy.”

As sire selection became more intentional, however, performance improved. By 2017–18, Cleveland says calves coming from dairy cows began to more closely resemble traditional beef calves. “We had to create animals that were going to perform,” Cleveland says. “And for us, that was really about focusing our genetic improvement to ensure we selected for the right things each segment wanted.”

Some of those genetic improvements included:

• Fertility and calving traits for dairies

• Feed efficiency and growth traits for feedyards

• Carcass merit and consistency traits for the packers

According to Cleveland, these efforts have helped beef-ondairy calves perform more like native beef cattle. And by focusing on traits that matter for dairies, feedyards, and packers, the beefon-dairy animals that we know today are much more consistent and valuable.

Performance Trends from the Packer’s Rail

With beef-on-dairy calves now performing more like traditional beef cattle, packers see that consistency as essential for maintaining quality and keeping cattle moving through the system. “Beef-on-dairy is a very important thing for the beef industry right now, especially when we’re talking about capacity,” Hardcastle says. “We have to make sure we have a beef population that can meet our consumers’ demand.”

Importantly, he emphasizes that these animals are not bringing down overall standards in the beef industry. “They’re good for the consumer,” Hardcastle says. “Tenderness data shows they perform very well, making a positive impact. These aren’t just animals being blended in that lower beef quality; they actually help improve it.”

He references Cleveland’s remarks, highlighting how focused breeding and feeding approaches have contributed to stronger quality grades. “Over the past five years, we’ve seen quality grades continuously improve,” he says. “Back in 2021, these animals graded 80% Choice or better. Today they’re leveling at about 92% Choice.”

Hardcastle says beef-on-dairy cattle are also making a notable contribution to Prime. “From a marbling perspective, almost twothirds of these cattle could qualify for upper two-thirds Choice,” he says. “The ones that don’t usually fall short because of factors like hot carcass weight, ribeye size, and fat thickness.”

From a carcass quality perspective, Hardcastle says beefon-dairy is delivering the kind of results the industry needs. They’re grading well, adding stability to supply, and proving they can hold their own in a system that demands both consistency and performance.

Processing Challenges Inside the Plant

Even as grades and marbling improve, processors are still working through carcass traits that affect returns, particularly excess kidney, pelvic, and heart (KPH) fat. Hardcastle explains that beef-on-dairy cattle often mirror their Holstein roots, tending to carry more KPH fat than native beef animals.

“From a packing perspective, you pay for a carcass with the kidney, pelvic, and heart fat in it, but that fat can’t be sold as beef,” Hardcastle says. “It ends up in the tallow market at 50 to 60 cents a pound, compared with about $3.60 on a beef grid, creating an immediate value loss.”

On today’s heavier carcasses, even modest differences in KPH can add up. “If I have a 950-lb. carcass, which is pretty common today, that can mean about 12 extra pounds of internal fat

instead of saleable meat,” he says. “That difference can cost $30 to $40 per head.”

These carcass differences are also highlighting the limits of traditional yield grade assumptions. “Yield grade is meant to estimate how much salable red meat a carcass will produce,” Hardcastle explains.

Based on ribeye size, backfat, and carcass weight, beef-ondairy cattle should cut better than native beef, but yield grades often don’t reflect their true performance. “Yield grade and beefon-dairy really aren’t closely related,” he says. “Research shows that yield grading doesn’t reliably predict cutability or value for Holsteins or beef-on-dairy cattle.”

This mismatch shows that standard measures like yield grade, internal fat, and weight don’t always capture the real value of beef-on-dairy animals, making it challenging for processors to price and sort them at the rail. To address this, Cargill is testing new technology called SizeR to capture 3D carcass measurements at chain speed.

“So, we can evaluate the full composition of these animals, not just traditional ribeye and fat thickness,” Hardcastle says. “This will help feeders and geneticists be able to better target the right traits to improve cutability and consistency.”

Growing and Permanent Force

Each year, millions of beef-on-dairy calves enter the market, providing a reliable source of high-quality cattle that deliver value from the dairy all the way to the packer. “We have somewhere in the neighborhood of 3 [million] to 3.5 million beef-on-dairy calves in the market today, which obviously represents a significant proportion of that beef supply chain,” Cleveland adds.

That presence is prompting both dairy and beef participants to think differently about their place in the larger system. “At every stage, from the dairy to the feed yard to the packer, these animals are performing and adding value,” Hardcastle says. “We understand the significance of beef-on-dairy, and we know that beef-on-dairy is not going away.”

As the industry continues to refine how these cattle are evaluated and managed, beef-on-dairy is positioned to remain a dependable contributor to both supply and consumer demand. With ongoing genetic gains and strong beef demand fueling the engine, the sector is gaining momentum and becoming a permanent fixture in the beef supply chain.